New accounting procedures may now be elected that will likely serve to dampen reported earnings volatility for many companies that hedge with forward contracts or options and, crucially, apply special hedge accounting.

What does “special hedge accounting” mean, and why is it so important? When derivative contracts are used as hedges, they’re generally intended to mitigate the earnings impact of some associated hedged item. And with this orientation, it makes sense to reflect the two earnings effects, i.e., those of the derivative and those of the hedged item, in the same earnings reporting period. Special hedge accounting delivers this outcome, thus reflecting the economic intent of the hedge. Without hedge accounting, in most situations the two earnings effects would be reported in different accounting periods making the intent of the hedge less transparent.

Unfortunately, hedge accounting is not automatic. Applying it requires satisfying a number of prerequisites, one of which is demonstrating to the satisfaction of your auditor that the intended hedge is expected to be “highly effective” in offsetting the risk being hedged. This concept of offset is critical, and it’s also problematic for forward hedges and option hedges. That is, for economically well-functioning forward contract hedges and option hedges, changes in these contract values often won’t offset the risks being hedged.

All-in-one hedge

Consider the case of an all-in-one hedge, where the company enters into a forward contract that obligates the firm to take delivery of a commodity or currency at some future value date, at a stipulated forward price. This hedge unambiguously locks in the forward price for the hedger, thereby eliminating any price uncertainty. Economically, it’s a perfect hedge.

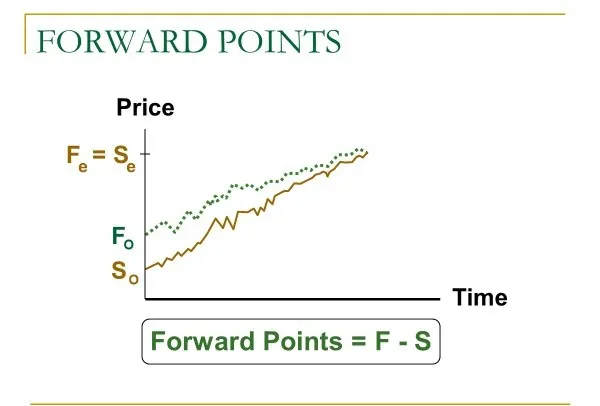

As a rule, prior to the forward’s expiration date, a forward price will almost certainly differ from today’s spot price, i.e., the price that would be required to buy that commodity and take possession imminently, But, as shown in the accompanying figure, forward (F) and spot (S) prices will converge as of the forward’s expiration date. Given this property of convergence, it should be clear that over the holding period of the forward contract, the spot price change (Se – So) will differ from the forward price change (Fe – Fo), with the difference being equal to the starting forward point amount. Unless addressed appropriately in the hedge documentation, this imperfect offset could jeopardize the capacity to apply hedge accounting despite the fact that this hedge perfectly locks in the original forward price on the forward contract.

In a similar vein, an option having the same underlying asset as the exposure being hedged might also provide a perfect economic hedge, assuring that the effective, all-in price (inclusive of hedge results) will be no worse than the option strike price, plus or minus the price paid for the option—plus if the hedge is a call option designed to protect a purchase price, minus if it’s a put option designed to protect a sales price.

With options, it’s important to understand that the price of an option can be composed of two components: the intrinsic value and the time value. Consider the case of the right to buy widgets (i.e., a call option) at a strike price of $50, when widgets are selling at $52 in the spot market. With this hedge in place, no matter how high the price of widgets might reach in the spot market as of the time the purchase is required, the hedger is assured that his/her worst case would be buying the widgets at the strike price of $50, plus the initial cost of the option. On the other hand, if the price of widgets falls below $50 by the intended purchase date, this hedger would allow the option to expire (or else liquidate the contract) and stand to enjoy an effective price that would be cheaper than $50.

In this example, the option’s intrinsic value is $2—the beneficial difference between the strike price and the spot price of the widgets from the point of view of the option buyer. With time remaining until expiration, the overall price of the option would be at least this intrinsic value, and then some. In this example, if the full option price were $3 when initially purchased, the intrinsic value would have been $2, and the time value would have been the residual $1.

Ultimately, when an option expires, the time value will erode to $0, and the option will have a terminal value equal to its intrinsic value. Continuing with the example, if the price of widgets were to rise to, say, $55 by the time the option reaches expiry, the option would end up having a terminal (intrinsic) value equal to $5. The change in the spot price over that time would be $3 (=$55 – $52), while the change in the full option price change would be $2 (= $5 – $3)—an imperfect offset.

FASB allows reporting entities to untie these Gordian knots—the seeming accounting ineffectiveness while these instruments are performing as intended, economically—by permitting forward point and option time values to be excluded from the assessment of hedge effectiveness. This semantic election is often sufficient to allow the hedger to assert that the offsets are highly effective, thus permitting hedge accounting. Without this election that conclusion would not hold.

Returning to the forward hedge example, by stating in the hedge documentation that forward points would be excluded from the hedge effectiveness assessment, the company can compare spot price changes for both the hedged item and the hedging derivative. This offset would be perfect when hedging a currency exposure with a derivative with a common currency denomination or if hedging a commodity component. Not so, however, when hedging a full commodity price with a derivative, when a non-constant basis applies to the commodity price. In this case, satisfying some additional quantitative test would be necessary to qualify for hedge accounting.

Returning, again, to the option example, excluding time value effects allows the comparison of the change in the spot price for prices above $50 (i.e., 55 – $52 = $3) to changes in the option’s intrinsic value (i.e., $5 – $2 = $3). As before, this election, by itself, would likely be sufficient to allow for hedge accounting for certain hedges, but not necessarily all.

Amended guidance

In the pre-amended accounting guidance, those who made this election in cash flow hedging situations had been required to recognize the gains or losses on these excluded items in current income on the basis of the excluded items’ mark-to-market value changes. This treatment thus fosters some unintended earnings volatility. More likely than not, the magnitude of these earnings effects would tend to be quite limited and immaterial for excluded forward points, but these effects might be many times larger for option time values. However small or large these might be, to the extent that the hedger’s motivation was to minimize income volatility, this mark-to-market aspect of the accounting treatment has been seen as a negative.

Many companies have been able to sidestep this problem by appealing to alternative hedge assessment comparisons.

For forward hedges, for instance, FASB allows the effectiveness assessment to compare the forward price implicit in the exposure to the forward price of the derivative, such that forward points are never explicitly excluded.

A similar workaround exists for option hedges, as well, under the terminal cash flow methodology. Under this method, the effectiveness assessment for an option hedge focuses attention on the final payoff of the option, relative to the intended risk being hedged. In effect, without saying so, this method also excludes the time value of the option as that final payoff is entirely intrinsic value. In any case, for cash flow hedges, the terminal cash flow method under the amended accounting guidance allows for the entire gain or loss on the option—both time value and intrinsic value—to be deferred initially though other comprehensive income (OCI) and later reclassified to earnings coincidentally with the earnings impact of the hedged item.

The guidance thus allows for two alternative ways of accounting for forward points or option time values. When these amounts are excluded from hedge effectiveness assessments, the excluded amounts are recognized in earnings throughout the horizon of the hedge. Without adopting this election, forward points and/or time value effects could be concentrated and reflected in earnings at or after the date the hedge terminates, in the period (or periods for caps and floor hedges) in which the hedged item affects profits. Conceivably, then, the exclusion method allows for spreading these earnings effects from forward points or time values over many accounting periods, albeit with some degree of income volatility, while the alternative approach concentrates the earnings recognition is the period in which the deferred gains or losses are reclassified.

In the pre-amendment world, many hedgers preferred not to exclude forward points or option time values from their assessment of hedge effectiveness largely because of an aversion to unintended earnings volatility during the hedge horizon. With the amended standard, however, FASB instituted a change that will likely alter the calculus. Specifically,

the new rules now permit the allowable excluded items (forward point effects and option time value effects) to be accounted for in any “systematic and rational method” devised by the reporting entity.

For most, this new allowance likely means that companies will choose to exclude forward point and/or time value effects. Instead of realizing these effects in earnings a market basis, though, they’ll recognize these amounts using straight-line amortization. The problem of unintended earnings volatility has been solved!

One caveat:

For entities that want to take advantage of this new flexibility to spread their hedging costs over multiple periods without introducing any unintended volatility, it’s important to realize the combined amount recorded in earnings and OCI must be identical to the total gain or loss of the derivative in every period. Thus, if the earnings impact from any excluded item is determined on the basis of some rules-based algorithm, the balance of the market value change of these excluded items would necessarily have to be posted to OCI—both for fair value and cash flow hedges. (It may be interesting to note that requiring any OCI allocation in connection with fair value hedges is an innovation that may not have been widely anticipated.) Those excesses and shortfalls will be fully offsetting by the end of the process, however, provided the derivative is not terminated or offset prior to its natural maturity. However, if and when derivatives are terminated early and excluded items have been allocated to earnings mechanically, a special final reclassification adjustment would likely be necessary to assure that the aggregated earnings realized for the derivative is identical to its market gain or loss.